How to Get Out of Debt

Having debt can feel scary, embarrassing, and lonely. Since most people don’t go around talking about their mound of debt and their plan for it, it can feel like you’re the only person in the world experiencing these feelings. Once payday comes, you may have little leftover after you pay your standard bills and minimum debt payments. Working so hard every day to then have no money left to do anything else is not a fun feeling.

But since misery loves company, I’ll share this stat with you, proving that you’re not alone: According to the US Department of Labor, around 77% of American households have some debt.

Yep! So now that you know you aren’t on your own Debt Island, let’s talk about how you can get out of debt once and for all!

Step 1: Organize your debt

How to organize your debt

First things first: We have to face it head-on. I want to stress the crucial nature of this step, even though it may not be the most enjoyable. It's the foundation of your financial journey, and it's essential for your future financial stability — I promise!

Grab your laptop—or a pen and paper; this doesn't have to be fancy—and list all your debts, including the due date, minimum payment due, and interest rate (also called Annual Percentage Rate, or APR). This will help you organize by knowing what's due and when it's due so you don't miss any payments.

If you don't know the due date, minimum amount due, or interest rate, call the company. As a fellow millennial, I know that calling someone on the phone doesn't rank high on the fun scale, but you have to power through and get this information.

Step 2: Set up autopay

Effective strategy for managing credit card debt is to set up autopay

Now that we have a list of our debts laid out, how are those due dates looking? If the due dates don't work with your pay schedule, call the company and ask to change the due date. Yes - you can do that! If you have several debts, consider spreading them out so some are due on one payday, and some are due on your other payday. But don't forget to take other large expenses into consideration, like rent, when you do this. You want to make sure you'll have enough money to actually pay that bill.

To take this a step further, set up autopay for the minimum payment on all your debts (and other bills while you're at it). Life is busy enough without remembering every bill's due date. I know this can feel terrifying if you have a lot of debt — we're just doing the MINIMUM payment here, not the total balance. And since we're setting it up to come out on your payday, you should have the funds to cover it. On-time payments are crucial when it comes to building credit scores; doing this can be a game changer. Missing a payment due date not only means you're hit with obnoxious fees, but it can significantly impact your credit score, which will follow you along for years.

Step 3: Choose a debt payoff method

Debt Payoff Methods

Now that we’ve established a solid foundation, it's time to get down to business. You can do one of three methods: snowball, avalanche, or a combo.

Snowball Method

The Snowball Method involves paying off debts in order of smallest balance and working our way up… kind of like a snowball getting bigger and bigger as you add more snow!

With this method, you pay the minimum on all debts (we ALWAYS do this, regardless of what method we choose) and put extra money towards the debt with the lowest balance until it’s completely paid off, working our way up to the highest. We can return to our handy dandy sheet, listing each of our debts and seeing what we will target first.

This method is excellent for those who know they will thrive with quick wins. After all, the smaller the debt, the faster you’ll pay it off!

Let’s look at this example below. With the Snowball Method, you’d pay off Credit Card 1, then Credit Card 3, then Credit Card 2… because that’s the order with the smallest balances.

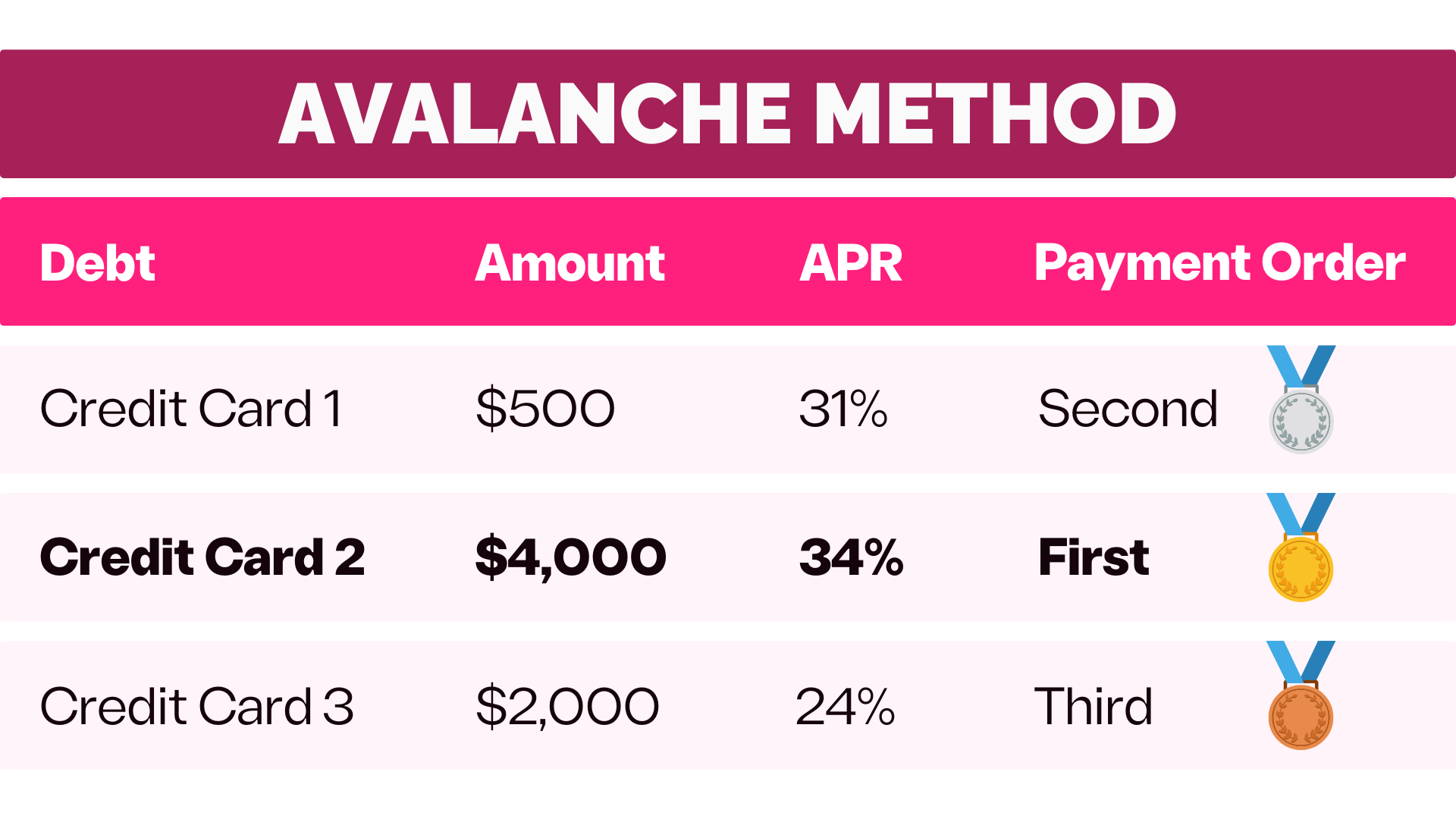

Avalanche Method

The Avalanche Method involves paying off debts in order of highest interest rate (APR) and working our way down… kind of like an avalanche starting at the top of a mountain and sliding down!

With this method, you pay the minimum on all debts and put extra money towards the debt with the highest interest rate until it’s completely paid off, working your way down to the debt with the lowest interest rate. So, we’ll want to return to our sheet listing our debts and interest rates and see what we will target first.

From a mathematical standpoint, this method is the best because it saves the most money on interest over time. The higher the interest rate, the more fees you’ll pay.

Let’s look at the example below. With the Avalanche Method, you’d pay off Credit Card 2 first, then Credit Card 1, then Credit Card 3…because that’s the order with the highest APR.

Combo Method

I don't think the Combo Method is technically a method, and maybe I made up the name, but it's my favorite.

This is where we flip-flop between the Snowball Method and the Avalanche Method. I like this because it lets you do what works best for you. For example, maybe you've been trying to pay off this debt for a while but haven't made any progress. You have a small balance on one card with a lower interest rate, and you know it would make sense to throw money towards a higher interest rate, but you think it'd feel good having one less card to worry about. Do that one! Just knock it out! Then, you can switch to prioritizing the higher interest rates.

Let's look at an example below.

Example: Maybe you have three credit cards:

Credit Card 1 has a $500 balance with a 31% APR

Credit Card 2 has a $4,000 balance with a 34% APR

Credit Card 3 has a $2,000 balance with a 24% APR

With the Combo Method, maybe you decide to use Credit Card 1 since it has a low balance and you want a quick win, but then maybe you use Credit Card 2 next since it has a much higher interest rate than Credit Card 3. You flip-flop between the two methods.

And guess what: the rules are fake. Try out one method and just switch if it isn’t working for you.

The only thing you DON’T want to do is just blindly throw money at debts randomly. Doing this means you get zero quick wins, which can feel really defeating when it seems like you’re making no progress.

You know yourself best. Since we are humans and not robots, it’s okay to take your feelings into account when paying off debt. If you know that you’d be most incentivized by knocking things off your list quicker, maybe you go with the Snowball Method. If paying fees and interest is keeping you up at night, try the Avalanche Method.

Benefits of Paying Off Debt Sooner

Paying off your high-interest debt as soon as you can can be life-changing. Notice I said HIGH INTEREST. I don't believe all debt is bad. If you're financing your car at a 2% interest rate — do your thang, my friend! But if you're rocking 30% interest rates on your credit cards, that's another story — it is destroying your bank account.

Knocking out your high-interest debt will save you money on interest payments and fees. Plus, paying off your debt will improve your credit score (which is important for buying a home or car, getting approved for large purchases, or even renting your dream apartment).

But most importantly, paying off your debt sooner will reduce your stress levels. Think about it: no more late-night stress sessions worrying about how you will pay your next bill, no more sleepless nights, and no more sick feeling in your stomach when it comes time to open your bank app. Money is mental AF. You work way too hard for your money not to prioritize you. The time has come to do it!

Other Helpful Tips for Getting out of Debt

Here are some other tips that may be helpful to you as you start to pay off your debt:

🪄You may consider calling your credit card company and seeing if they can lower the interest rate. They may be willing to (at least temporarily) if you have a good payment history.

🪄Call your credit card company to see if they have any special promotions they can offer you. The worst thing they’ll say is no 🤷🏼♀️

🪄Building a “fun” piece to your budget and having an emergency fund should be non-negotiables. You don’t have to cut out everything! If your morning Starbucks is the best part of your day, keep it in your budget! Will it delay your debt-free date slightly? Probably. But don’t treat your debt-free journey like a financial diet pill. It’s better to create something sustainable that you will stick to than fall off the wagon a few months into your journey.

Wrapping Up

Taking the first step is the most challenging but crucial part of your debt-free journey. You have to face it head-on. It doesn’t go away just because we aren’t looking at it. Lame, I know.

Debt can also invoke a lot of big feelings. I beg you not to beat yourself up, though. You can’t go back in time, but you can start moving forward now. Follow the plan and stick to your commitment, but also be patient with yourself. You will fall off the wagon, and your first plan won’t be perfect, but get back on that wagon. You owe it to yourself and deserve to get back on it!

I won’t lie to you and say that becoming debt-free isn’t a challenging journey, but I can tell you it is the most fantastic feeling. I still remember how I felt when I made my last student loan payment. Sitting in my apartment alone, I suddenly looked around for someone to high-five. WHY IS CONFETTI NOT EXPLODING OUT OF MY COMPUTER?🙂

You can do hard things. I know it. If you pay off your debt, let me know, and I would love to give you a virtual high five!

Looking for even more money management tips to crush debt and build wealth? Join the Wolfe Pack and get my newsletter to be delivered right to your inbox each week!