Should I Max Out My 401k or Payoff my Student Loans?

A common question I get is whether you should prioritize maxing out your 401k or paying off student loans. The Investing Order of Operations can be a bit tricky because it’s so circumstantial, but there are a few things I recommend doing in a particular order, no matter what, so that you maximize your money (because we want to keep as many of our dollars as possible).

One of the most common dilemmas many people face is whether to prioritize saving for retirement by maxing out their 401(k) or paying off their student loans before throwing extra money toward retirement savings.

Not to be hyperbolic, but this is a pretty important decision that can significantly impact your long-term financial well-being. No pressure or anything 😅.

5 Things to Consider When Deciding to Max Out 401k When in Debt

1) Interest Rates and Debt Amount

The first thing you want to consider in the 401k vs. student loans debate is the interest rate on your student loans. Interest rates can vary widely, and it's essential to understand the cost your rate(s) have on your debt. If your student loans carry high interest rates (the general rule of thumb is anything higher than 8%), it makes more sense financially to pay off that debt as soon as possible.

High-interest loans really suck in the long term. The interest payments add up quickly, and you could end up paying significantly more than the original loan amount over time. For high-interest student debt, prioritizing debt repayment over maximizing your 401(k) contributions may be the right approach.

However, if your student loans have relatively low interest rates (less than 8%), it may make more sense to continue making regular payments while investing in your 401(k). By investing, you have the potential to earn a return that outpaces the interest you're paying on the loans. After all, the average return of the the stock market is 10-11% (8% when you account for inflation which is where we get that general rule of thumb number mentioned earlier).

2) Employer Match

Many employers offer a 401(k) matching program as part of their benefits package. This is as close to free money as you can get, and it's one of the most appealing reasons to contribute to your 401(k). If you don't contribute enough to your 401(k) to get the full employer match, you're essentially leaving money on the table (and really leaving part of your salary on the table as your HR team definitely took that into account when offering you your job!).

We hate to see it.

To show you an example:

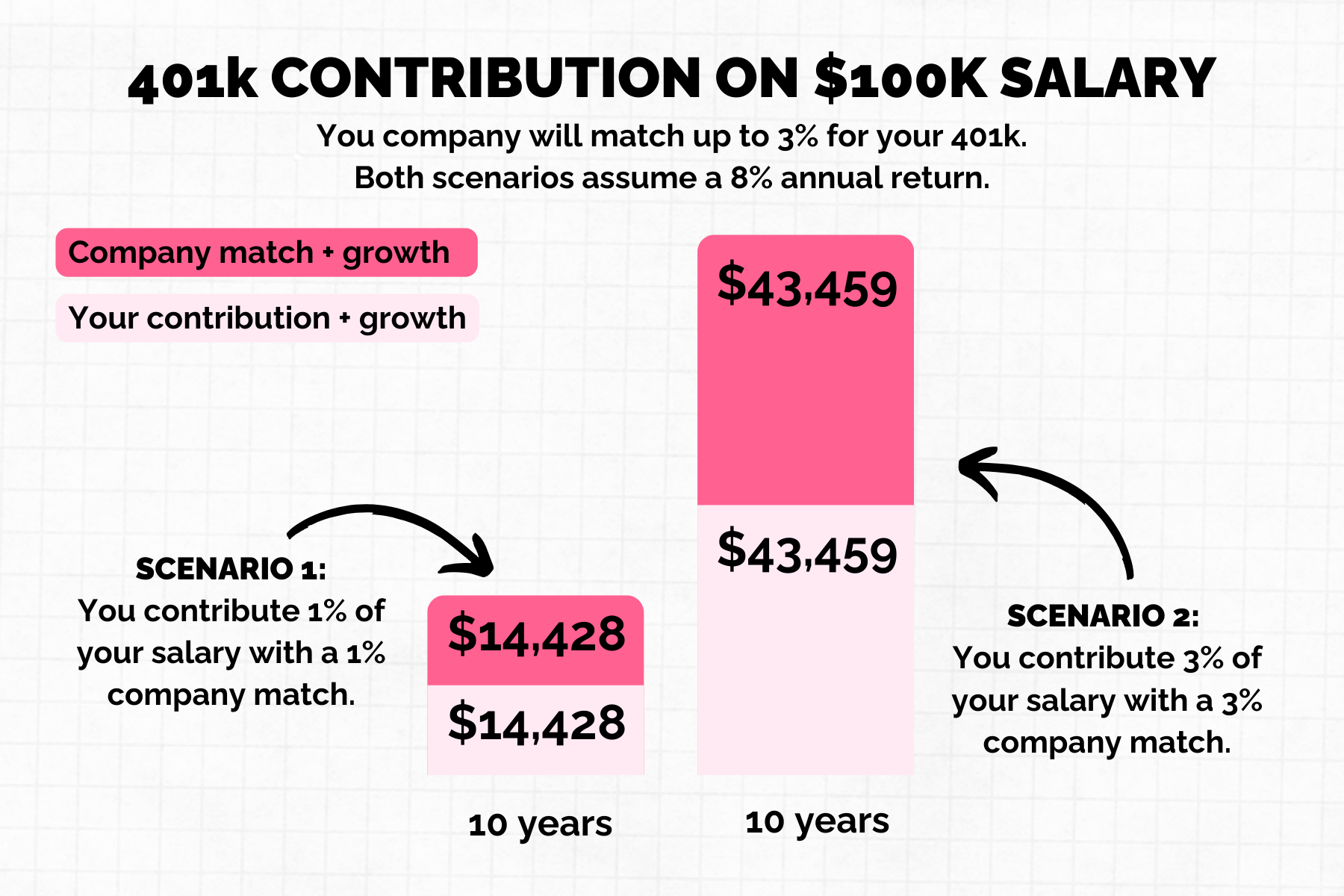

If your employer offers a 3% match and you only contribute 1% of your salary, you're missing out on a 2% contribution from your employer. That's a 100% return on your investment without any market risk!

The chart below shows an example of the potential growth over just 10 years if you made $100,000/year and contributed at least 3% of your salary to get the full company match vs contributing only 1% of your salary. Look at all that money you miss out on from your employer!

Therefore, even if you have student loans, you want to make sure you’re contributing enough to your 401(k) to at least maximize the employer match.

3) Timeline for Retirement and Debt Repayment

Your age and the timeline for both retirement and debt repayment are important factors to consider when thinking about what’s the best use of extra $$$ in your monthly budget.

If you're young and have several decades before you plan to retire, time is on your side. If you’re not planning to retire for years still, prioritizing your 401(k) can be advantageous. Investing early allows your money to benefit from the power of compound interest.

Over time, even small contributions can grow substantially.

However, if you're closer to retirement or if the interest on your student loans is a substantial burden, it may be better to focus on paying off the loans. Reducing debt will free up more of your income for other financial goals and reduce financial stress as you approach retirement. Because after all, retirement is supposed to be enjoyable.

It's so important to strike a balance between saving for retirement and paying off debt (and this is easier said than done, I know). I’m a big fan of a financial plan that includes both elements.

4) Risk Tolerance

I’m always talking about mentality around money and when it comes to deciding to invest more in your 401(k) or pay off your student loans. Money mentality is super important and so is knowing your own risk tolerance.

Consider your risk tolerance and how the debt makes you feel. Our 401(k) investments will likely fluctuate up and down over the years. So you may think, student loans it is! But ALSO, we know that our investments need time to work. In that case, investing in our 401(k) it is! And then we’re back to square one, still stuck in our decision process.

Paying off student loans may provide a sense of financial security, as it eliminates a (stressful AF) financial obligation. If they are keeping you up at night, despite a lower interest rate, it’s okay to focus on those even if it doesn't make the most financial sense. Or if they’re high interest loans, but it’s stressing you out not investing at all during this pay off period, it’s also okay to invest a little somethin’ somethin’ as you pay them off too.

Whatever route you go, just make sure investing comes into play at some point or we’ll be shooting our future rich girl selves in the foot by not doing so. And we don’t deserve that kind of treatment.

5) Tax Considerations

Traditional 401(k) contributions are generally tax-deductible, which can lower your taxable income. By reducing your taxable income, you may pay less in income tax each year. This tax benefit can provide you with some immediate savings.

However, there may be tax implications for your student loans as well. In some cases, the interest paid on student loans may be tax-deductible, providing another avenue for potential tax savings.

In general, I am not an accountant, so I won’t even attempt to advise anyone on their taxes. But I DO want you to feel empowered to look into it and have a seat at the table. Because there are tax implications for both sides of this debate, I highly recommend consulting a tax professional to get advice on your specific situation.

Wrapping Up

Like just about everything else in the world of personal finance, the decision isn't an all-or-nothing proposition. Try to strike a balance by prioritizing contributing to your 401(k) in order to get your full employer match (if available), and then allocating additional funds to pay down your student loans. With this approach, you can save for retirement while also managing your debt.

As you make progress in paying off your loans, you can then increase your 401(k) contributions.

A serious win-win!